What's the Best Medicare Supplement for You in 2023?

When you start looking at Medicare options, it can seem overwhelming.

Don't despair! Today, we're going to break down Medicare Supplements so you will know how to figure out which one is the best option for you if you choose a Medicare Supplement for your health coverage. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To... What Are Medicare Supplements?

Medicare Supplements, also known as Medigap plans, are insurance policies that fill in the gaps that would otherwise be your out-of-pocket costs in Original Medicare, Parts A and B.

Medicare Parts A and B are your primary insurance coverage. If you have a covered medical expense, Medicare pays its responsibility first, then your Medicare Supplement pays based on the plan’s benefits. Medicare Supplements are much older than Medicare Advantage Plans and Medicare Part D plans and have different rules and laws governing them. Why would you choose a Medicare Supplement for your coverage?

If you have a Medicare Supplement, you don’t need to worry about provider networks because, if you have a standard Medicare Supplement, there are no networks. You can see any medical provider who accepts Medicare. This makes Medicare Supplements popular with people who don’t want their choice of doctors restricted by an insurance company.

You also don’t have to worry about benefit changes. Insurance companies can’t make any changes to Medicare Supplement benefits. These plans are standardized by law, so the only time benefits change is when a new law changes Medicare Supplements across all companies. Also, there’s no need to take time to compare Medicare Supplements during the Annual Enrollment Period between October 15 and December 7 because Medicare Supplements are not affected at all by the Annual Enrollment Period. They are month to month contracts that you can change any time during the year. The rules for changing Medicare Supplements do vary from state to state and can depend on your health and how long you’ve been on Medicare. If you are beyond your first six months on Medicare Part B and don’t have a guaranteed issue right, you will have to answer health questions and go through underwriting to be able to purchase a new policy. For most people, that isn’t a barrier to changing. More information on Medicare Supplement underwriting can be found in the video linked here: https://youtu.be/br-4S0U912U.

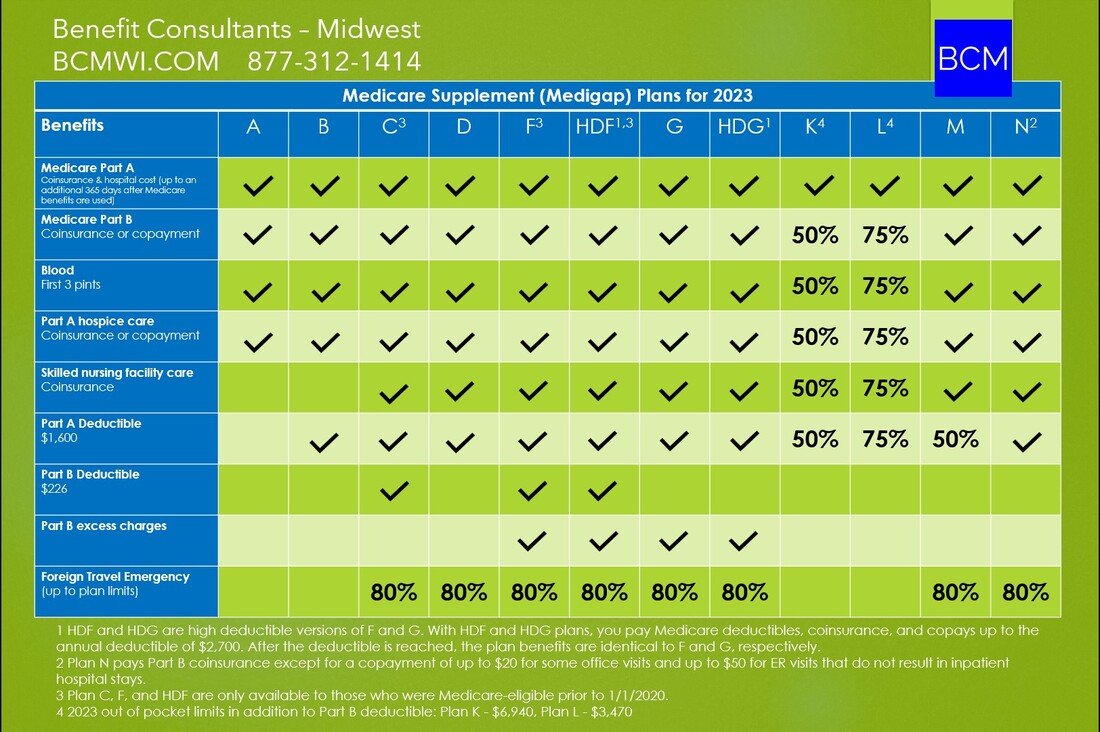

Medigap companies have to offer Plan A, and beyond that, each company chooses which other plans (B, C, D, F, HDF, G, HDG, K, L, M, N) to market in each state.

Some of the plan designs don’t make much sense financially for Medicare beneficiaries, so very few insurance companies even offer them. That’s the case with B, D, K, L, and M. Also, Plans F and C are only options for people whose Medicare Parts A and B effective dates are before Jan 1, 2020. Even if you have been on Medicare long enough to be eligible to purchase a Plan F, it’s not a good idea. More on why that is in the video linked here: https://youtu.be/M81-iDbIfpo. After those eliminations, the plans that offer the best value for consumers are Plan G, Plan N, and High Deductible Plan G. Let’s look at each of these in detail. Medigap Plan G

Plan G is the most comprehensive Medigap plan of the three. For all medical care covered by Medicare Parts A and B, your out-of-pocket risk with a Plan G is limited to the Part B outpatient annual deductible. In 2023, this deductible is $226.

If you reach that deductible, all outpatient expenses beyond that are covered between Medicare Part B and Plan G at no cost to you. This includes things like office visits, diagnostic testing, and all outpatient treatment. On the inpatient side, all covered expenses are split between Medicare Part A and Medigap Plan G. You have no out-of-pocket deductible for inpatient care. Because Plan G has the most coverage with the least risk of out-of-pocket spending for you, it is the most expensive of these three Medicare Supplement options. Since Medicare Supplement prices generally go up once a year as you age, we need to think about future costs in addition to the initial price when you first apply. Plan G is more expensive when you first enroll, and you can expect yearly increases in the premium to be larger than what a Plan N or High Deductible Plan G will have. Who should consider Plan G?

If you have very expensive, ongoing treatments like chemotherapy, treatment for rheumatoid arthritis, or any other medical condition that needs regular or costly care, a Plan G can be a good choice for you.

That higher Plan G monthly premium is balanced out by the savings in out-of-pocket costs because you don’t have a big deductible to meet or any copays. High Deductible Plan G

At the opposite end of the coverage spectrum, we have High Deductible Plan G. This Medicare Supplement provides exactly the same coverage as Plan G, with one big difference: You have to meet a high deductible before the High Deductible Plan G will pay anything.

In 2023, that deductible is $2,700. If you have a High Deductible Plan G, you pay the Medicare Part A and B inpatient and outpatient deductibles, copays, and coinsurance up to $2,700. If you reach that amount in your spending, then the Medicare Supplement kicks in and pays just like a standard Plan G. Because this plan has the least amount of coverage and the biggest out-of-pocket risk for you, it has the lowest monthly premium cost. High Deductible Plan G also has the smallest premium increases every year. Who’s an ideal candidate for a High Deductible Plan G?

If you are healthy and don’t need much medical care, this can be a great way to protect yourself from catastrophic medical charges while saving a ton of money on monthly Medicare Supplement premium costs.

In many parts of the country the difference in the premium between a Plan G and a High Deductible Plan G is well over $100 per month. High Deductible Plan G rates also increase much more slowly than Plan G or Plan N rates. Why not just have Original Medicare Parts A and B? Do I need a Medicare Supplement?

Medicare Parts A and B have no out-of-pocket spending limit for beneficiaries.

If you only have Medicare Parts A and B, there’s no limit to how much you can spend for your medical treatment in a calendar year. A High Deductible Plan G provides a cap on what you can spend in a year, and if you have a serious illness or injury, you have the assurance that your spending, in addition to monthly premium costs, won't exceed $2,700 for the year. Medigap Plan N

Then, in the middle of the coverage options, we have Medigap Plan N. This is a newer Medicare Supplement plan, and it grows in popularity every year. It is like G but slightly less comprehensive.

Because Plan N has middle of the road coverage between Plan G and High Deductible Plan G, it also has middle of the road premium costs. There are two differences between G and N. Both are in the outpatient coverage. Inpatient coverage is identical between G and N. Medicare Part B Excess Charges

One difference is that Medicare Part B Excess Charges are not covered by Plan N. In most cases, that’s not a big concern.

The only time you can be billed an excess charge is if you see a doctor who contracts with Medicare as a non-participating provider. Only about 4% of Medicare providers contract with Medicare as non-participating providers. A non-participating provider accepts Medicare patients but doesn’t accept Medicare payments as payment in full and can balance bill patients up to 15% more as an excess charge. To find out how your providers are contracted with Medicare, you can use the Physician Compare tool at medicare.gov. Of course, the easiest way to avoid excess charges is to only use providers who contract with Medicare as participating providers. If you must use a non-participating Medicare provider, how often can you expect excess charges to show up on your bill? A few years ago, one of our Medicare Supplement insurance companies looked at all their claims for one year and found that 99.34% of claims had no excess charges. Of the 0.66% of claims that did include excess charges, the average cost of an excess charge was under $20. Excess charges are rare, and they aren’t automatic if you are seeing a non-participating provider. The provider can decide whether to balance bill a patient on a case by case basis, and the amount is not always an extra 15%. The rule is the excess charge can be up to 15%, so it may be less. The risk of excess charges is so low that paying extra for a Medigap plan that covers excess charges generally doesn’t make much sense. Outpatient Copays

The other difference between G and N is that with Plan N, after meeting your Part B outpatient deductible for the year, you may have copays for office visits of up to $20 and for ER visits of up to $50, although that’s waived if you are admitted to the hospital.

These office visit copays are not charged at every visit. It depends on how your visit is coded by your provider’s office. So, it isn’t guaranteed that you will have any copay at an office visit, but if you do, it is capped at $20. How to Choose Between Medicare Supplement Plan G and Plan N

If you’re trying to decide between a Plan G and a Plan N, look at the difference in the premium cost between the two plans in your zip code and estimate how many office visit copays you are likely to pay in a year.

Premiums vary widely from one state to another. Here are a couple quick examples from rates in Illinois. For a male, age 70, a Plan N has a premium savings of about $35 per month over a Plan G, for a total of $420 per year. If he makes fewer than twenty office visits per year, the Plan N is the better value. For a female, age 70, Plan N saves about $30 per month versus Plan G, for an annual savings of $360. If she makes fewer than eighteen office visits per year, Plan N is the better financial value. Remember, there are also future costs to consider when choosing a Medicare Supplement. Because Plan N has slightly more out-of-pocket risk for policy holders, the rates increase more slowly than Plan G premiums. Comparison Shopping Medicare Supplements

Once you’ve decided on the Medicare Supplement Plan that has the right level of coverage for you, it’s time to comparison shop all the companies that offer that plan in your area.

Although the coverage is standardized by law, the costs from company to company for the exact same plan are wildly different. Different companies use different pricing models, so it is really important to do detailed comparison shopping and research before applying. It can save you a lot of money initially and in future years. This is what we do for all of our clients as Medicare plan brokers. We work with many insurance companies and can impartially comparison shop with you to find the plan and the company that’s the best fit for your situation. We do this completely free of charge to our clients. We’re able to do that because for every enrollment into a Medicare plan through our office, we are paid a commission by an insurance company. The commissions are similar across plans and insurance companies, so we have no reason to push one company over another for our own gain. We are free to find the plan and the company that fits each client’s medical and financial situation best. The Medicare plan cost to you is the same whether you buy direct from an insurance company or purchase through a Medicare plan broker. Once you are a client of ours, you have ongoing free access to expert help whenever you have a question about your coverage or when premiums or plans change and you need to re-evaluate and possibly switch Medicare Supplement policies. If you have Medicare Supplement questions, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. We’re here to help you understand your options and find the best Medicare plan for you!

0 Comments

Best Medicare Plan for 2023: Medicare Supplement OR Medicare Advantage?

Medicare is confusing!

There are so many different options for coverage, and in the months before you turn 65, you get a mountain of mail from every insurance company out there claiming their Medicare plans are the best. You can ignore all of that. Here’s how to find what’s best for your Medicare coverage. This is helpful if you’re turning 65 soon or if you chose a Medicare plan years ago and it’s time to review your choice to make sure you’re still in the right plan and not paying more than you need to. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To... Medicare Supplement OR Medicare Advantage

Most people have two major options: Original Medicare Parts A and B plus a Medicare Supplement, which is also known as a Medigap plan, and a Medicare Part D plan OR a Medicare Advantage plan that includes Medicare Part D drug coverage.

Choosing one of these is the first step in finding the best Medicare coverage for you. Let’s take a look at which of these options will work better for you. Medicare Part B

First, no matter what Medicare coverage you choose, you will have to pay your Medicare Part B premium. In 2023, most people pay $164.90 per month for Medicare Part B.

This is income dependent. High income individuals pay more than the standard premium, and folks with low income may pay less. Include that cost in any estimate of healthcare expenses. No Medicare Plans are FREE

It’s important to mention that no Medicare plans are free.

You will pay for healthcare in different ways depending on your plan choice, but no Medicare option free. Paying for Healthcare: Medicare Supplement vs Medicare Advantage

Here’s the big difference in how you pay for healthcare with a Medicare Supplement plus standalone Part D plan versus a Medicare Advantage plan.

If you choose a Medicare Supplement and Part D plan, you will have additional monthly premiums you will pay to remain enrolled in each of those plans. For a more comprehensive Medicare Supplement, those premiums can be well over $100 per month. The prices vary quite a bit depending on where you live and your age. The trade-off for paying those higher premiums is when you go to the doctor or the hospital, you will have very low or no out-of-pocket costs for the medical treatment you receive. For example, if you purchase a Medicare Supplement Plan G, your out-of-pocket costs for Medicare covered medical treatment is capped at $226 in 2023. Medicare Advantage plans are the opposite. Many Medicare Advantage plans have $0 monthly premiums. They’re able to charge you nothing to be in the plan because Medicare pays a contracted amount every month to the Medicare Advantage plan to manage the health care of each person who enrolled in that plan. With a Medicare Advantage plan, if you need to see a doctor, go to a hospital, or receive any kind of medical treatment, that’s when you have to pay. There are set copays and coinsurance percentages that you pay during the year for healthcare you receive. Every Medicare Advantage plan has an out-of-pocket spending limit for the year to protect enrollees’ finances. If you pay that much, then the insurance company will pay all of your covered medical costs for the rest of the year. When it comes to drug coverage, you will pay a copay or coinsurance with either coverage option when you pick up medications. That’s the big difference in how you pay for healthcare with these two options. Let’s look at coverage differences. Will I Have Original Medicare Coverage?

Original Medicare is Medicare Parts A and B.

Medicare Part A is inpatient insurance. Medicare Part B is outpatient insurance. Whether you choose a Medicare Supplement or a Medicare Advantage plan, you have full Original Medicare Parts A and B coverage. By law. If you have a Medicare Supplement, Original Medicare is your primary insurance and the Medicare Supplement pays costs that would otherwise be your responsibility, like deductibles, copays, and coinsurance. Medicare Advantage plans are required to cover at least as much as Original Medicare and that standard is checked and approved for each plan every year before it’s allowed to be offered to the public. Virtually all Medicare Advantage plans offer coverage beyond what’s covered by Original Medicare. If you choose a Medicare Advantage plan, that plan is your primary health insurance, rather than Original Medicare. Are There Medical Provider Networks?

With a standard Medicare Supplement, there are no provider networks. You can see any doctor and go to any hospital that accepts Medicare.

Medicare Advantage plans do have provider networks. Some Medicare Advantage plans will only cover your care if you see an in network provider. Other plans will cover medical care from out of network providers, usually at a higher cost to you. It is very important that you make sure all of your doctors are in a plan’s network before enrolling so you don’t get surprise bills later. Is Coverage the Same from One Plan to Another?

Medicare Supplement coverage is standardized by law.

However, monthly premium costs and underwriting are very different from one company to another. It’s important to comparison shop. Medicare Advantage plan coverage is not standardized, so you do need to look at each plan individually to make sure it’s a good fit for you before enrolling. How Claims are Processed: Medicare Supplement vs Medicare Advantage

There’s also a big difference in how claims are processed between these two options.

With a Medicare Supplement, your provider submits a claim for medical services to Medicare itself. Medicare determines if the claim is covered, and if it is, Medicare will pay its part and send it on to the Medicare Supplement company, which will pay its part. Medicare Supplement insurance companies can’t argue with claim decisions made by Medicare. This saves you time and hassle because it means you’ll never have to argue with your Medicare Supplement company about a claim. All those decisions are made by Medicare. Medicare Advantage claims are determined by the Medicare Advantage company. All of these plans have to include coverage that is as good as or better than Original Medicare, but the costs to you are not identical to Original Medicare. It’s important to look at each plan’s copays and coinsurance costs for medical services, and know what the process for disputing a claim decision is before enrolling in any Medicare Advantage plan. Medicare Supplement or Medicare Advantage for You?

There is no one size fits all Medicare coverage.

If you prefer predictable monthly costs with few extra charges through the year when you receive medical care, take a look at Medicare Supplements. If you’d rather have low or even $0 monthly plan costs and pay for medical services as you use them, look at the Medicare Advantage plans in your zip code. Once you’ve narrowed your choice to one type of coverage or the other, there are still plenty of options open to you for either Medicare Supplements or Medicare Advantage plans. How to Shop for Medicare Plans

This is when you get down to comparing specific plans from specific companies.

For that, you will need tools like medicare.gov, insurance company websites, your state department of insurance website, Medicare publications, and insurance company documents. You can do all the research and comparison shopping between all available plans and companies on your own, but it’s time consuming, complicated, and can get frustrating. Plus, there’s absolutely no benefit to doing it on your own. Medicare plan costs are the same whether you put in all that time and work on your own and enroll directly with an insurance company or you enroll through a Medicare plan broker who does all the research and comparison shopping for you. Have Questions? We Can Help!

This is what we do for all of our clients. We work with many insurance companies and can impartially comparison shop with you to find the plan and the company that’s the best fit for your situation.

We do this completely free of charge for our clients. We’re able to do that because for every enrollment into a Medicare plan through our office, we are paid a commission by an insurance company. The commissions are very similar across plans and insurance companies, so we have no reason to push one company over another for our own gain. We are free to find the plan and the company that fits each client’s medical and financial situation best. Once you are a client of ours, you have ongoing free access to expert help whenever you have a question about your coverage or when premiums go up or the Medicare Annual Enrollment Period rolls around again, and it’s time to re-evaluate and possibly change plans. If you have Medicare questions, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. We’re here to help you understand your options and find the best Medicare plan for you. How to Prepare for the 2023 Annual Enrollment PeriodIn this video, we’ll go through what you need to do to prepare for the Medicare Annual Enrollment Period, which runs from October 15 through December 7. And we’ll get that done in under 5 minutes! Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

The Medicare Annual Enrollment Period from October 15 through December 7 applies to Medicare Advantage plans and Medicare Part D plans.

The Medicare AEP does not apply to Medicare Supplements, also known as Medigap plans. You can change your Medicare Supplement any time during the year, but you may have to answer health questions to be approved for a new policy. That’s true even during the Medicare AEP.

The advertising this time of year for Medicare Advantage and Medicare Part D plans is non-stop. Do you need to watch all the tv commercials, read everything you get in the mail, and listen to every sales pitch? No. You can safely ignore it all. The advertisements let you know what the latest bells and whistles are on some plans, but they don’t tell you which plan is the best one for you. What's the Best Medicare Plan for You?The best plan for you is the one that covers all your medications at the lowest cost and with the fewest restrictions, has all of your medical providers in network, and will provide you access to the healthcare you need for the new year at the lowest overall cost. Here’s what you need to do during the Medicare AEP:

That’s really all you need to do. Once you have your lists and other necessary information, it’s time to look at all available plans in your zip code. You can do that on your own, but it can be time-consuming and complicated. A licensed, experienced Medicare plan broker will assist you with the comparison shopping at no cost to you. Whether you purchase through a broker or directly with an insurance company, the plan cost will be the same, so why not take the free help from someone who is trained in this field and does this for clients every day? If you want to know more detailed information about the Annual Enrollment Period, including what plan changes you can make during the AEP, and what changes you can’t make, here's a link to another video that explains what options are available in more detail. If you’d like assistance sorting through your options for the new year during the Medicare AEP, please feel free to give our office a call at 877-312-1414 or or schedule a free, no obligation Medicare plan consultation. We’re here to help you have a stress-free AEP and make sure you are in the best Medicare plan for you. Have a great day! Medicare 2023 Part B Premiums NEW INFO RELEASED BY CMSCMS released the 2023 Medicare Premium and Deductible amounts on September 27. There’s some good news for Medicare costs with decreases in premiums and deductibles for 2023. Also, good news, they released this information much earlier than usual, so everyone can prepare going into the Annual Enrollment Period Oct 15 though Dec 7 knowing what 2023 Medicare Parts A and B costs will be. In this video, we’ll go through the new numbers and how they affect you. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To... Medicare Part B Premium & Deductible

In 2022, the Part B premium for most people is $170.10 per month. For 2023, that is decreasing to $164.90 per month, which is a decrease of $5.20 per month.

If you have higher income, a here is a link to the IRMAA charts for both Parts B and D for 2023. Remember, Medicare bases these amounts off your tax returns from two years ago. If your income has gone down in the last two years, you can appeal your IRMAA decision using more current financial information. Here is a link to the appeal form. Many of our clients have successfully appealed and gotten those IRMAA charges reduced or eliminated. New for 2023, if you are 36 months past a kidney transplant, you can elect to remain on Medicare Part B for coverage of immunosuppressive drugs, even though you aren’t eligible for full Medicare benefits anymore. That monthly premium is $97.10. More information on that benefit is available here. The Medicare Part B annual deductible is also decreasing from $233 in 2022 to $226 in 2023. Why did your Part B costs go down for 2023? From 2021 to 2022, Medicare Part B had its largest premium increase in history. Much of that was due to anticipated spending on the new Alzheimer's drug, Aduhelm. Spending on that drug and other Part B services was not as high as projected, so Medicare is lowering that Part B premium for 2023. Medicare Part A 2023 CostsMost people do not have to pay a monthly premium for Medicare Part A, which is inpatient insurance. Medicare Part A was paid for with your FICA taxes if you worked and paid those taxes for at least 10 years. Medicare Part A does have inpatient deductibles and coinsurance amounts, which are shown here. The Part A deductible is going up to $1,600 for 2023. The per day hospital and skilled nursing facility coinsurance amounts are increasing as shown. Annual Enrollment Periodthe Annual Enrollment Period is coming up October 15 through December 7. That’s the time you can change your Medicare Part D or Medicare Advantage plans. The AEP does not apply to Medicare Supplements, Plan G, Plan N, High Deductible Plan G, and so on. For more information on what coverage changes you can make during the Annual Enrollment Period, please see the video linked here. Have Medicare Questions? We Can Help!For answers to your specific Medicare questions and to objectively compare all available Medicare plans where you live, please feel free to call our office at 877-312-1414 or schedule a free, no obligation Medicare plan consultation. Our services are always free and enrolling through our office does not increase the cost of any insurance. Your 2023 Medicare Annual Enrollment Period Guide: Everything You Need to Know for AEP October 15th - December 7thThe Medicare Annual Enrollment Period is almost here again! Every year from October 15 through December 7, Medicare plans take over advertising everywhere. It’s impossible to ignore, but it isn’t always clear what the Annual Enrollment Period means for you. The video below will guide you through what you should do during the AEP, what you can do if you choose, and let you know which Medicare plans are affected by the Annual Enrollment Period and which plans are not. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To... Which Medicare Plans are Affected by the AEP?The Annual Enrollment Period occurs every year from October 15 through December 7 and applies to Medicare Advantage plans and Medicare Part D plans but NOT Medicare Supplements, also known as Medigap policies. For more information about Medicare Supplements and the Annual Enrollment Period, please see the video linked here. What should you do during the Annual Enrollment Period?1. If you are in a Medicare Advantage Plan or a Part D plan, you will receive an Annual Notice of Change by September 30. Take a little time to review the changes that your plan is making for the new year. Although the whole packet from the insurance company may be huge, there is usually a clear summary of changes document that is a good place to start. If the changes for the new year don’t affect you, you can stay in the plan by doing nothing during the Annual Enrollment Period from October 15 through December 7. Your coverage will continue in the new year. However, if you find yourself in this situation, it’s always a good idea to look at all plans being released in your area to see if any of them would be a better fit for you than your current plan, since they all can change every year. Medicare insurance companies and Advantage plans keep expanding into new areas, so it’s worth a quick check every year to see what’s new where you live. If you read your Annual Notice of Change and learn your current plan’s changes will affect you negatively, you should definitely look at other options in your zip code during the AEP. What to look for in your Annual Notice of Change:If you have a standalone Part D plan, check the monthly premium, the annual drug deductible, pharmacy network (Is your pharmacy still in network?), and your medications (Did the Tier level or copay change for any? Are there any new restrictions on your medications?) If you have a Medicare Advantage plan, check the monthly premium, any deductible amounts, the out-of-pocket maximum for the year, provider network (Are your doctors staying in the network?), and copay and coinsurance amounts for medical services you routinely use or expect to use in the upcoming year. If you are in a Medicare Advantage plan that includes Part D drug coverage (an MAPD plan), you’ll need to look at all of the above in your Annual Notice of Change. 2. Communicate with your doctor’s office. Some doctors and medical practices change networks from year to year or decide to only accept certain types of Medicare plans for the new year. If your doctor is doing this, you need to know during the AEP. What plan changes are you allowed to make during the Annual Enrollment Period?

Those are the things you can do during the Annual Enrollment Period. Whether you make any of those changes on October 15 or December 7 or any day in between, plan changes all become effective on January 1. One note: generally, you can’t enroll in both a Medicare Advantage plan and a standalone Part D plan at the same time. The only exceptions to that are some Private-Fee-for-Service plans, Medical Savings Account plans, Cost plans, and certain employer-sponsored Medicare health plans. What About Medicare Supplements during the Medicare Annual Enrollment Period?Medicare Supplements, also known as Medigap plans do not fall under the Annual Enrollment Period. These are much older plans that follow different enrollment rules. You can change your Medicare Supplement plan any time during the year. However, in most states, and under most circumstances, you will have to answer health questions and provide a list of your medications and pass underwriting in order to be able to purchase a new plan. There are exceptions based on state laws, and there are some guaranteed issue Medicare Supplement companies that accept everyone age 65 or older who has Medicare Parts A and B, but don’t assume that if you leave a Medicare Advantage plan and return to Original Medicare during the AEP that you will be able to purchase a Medigap plan. That’s definitely something to look into before leaving your Medicare Advantage plan. The health questions for Medigap underwriting do vary from company to company, so a broker will be able to assist you in finding a company that is likely to accept your application, if at all possible. If you are thinking of leaving your Medicare Advantage plan during the AEP and want to purchase a Medicare Supplement plan, start the process early. If you apply for a Medigap plan on October 15 with a January 1 effective date, which is the earliest you can leave your Medicare Advantage plan, you should have an answer with plenty of time left in the AEP to apply to a different Medigap company if necessary. What if you have a Medicare Supplement plan you’re happy with? Medicare Supplement plans are guaranteed renewable as long as you pay the premium and they do not change benefits from year to year. You do not need to do anything during the Annual Enrollment Period if you want to keep the Medigap plan you have. 2023 Medicare Insurance Plan Broker/Agent Communication ChangesTwo big changes are coming October 1, 2022 that will carry into 2023 regarding your communication with your Medicare plan agent or broker. The first change is that all phone calls between you and your Medicare plan broker that discuss Medicare Advantage plans or Medicare Part D coverage will have to be recorded and kept on file for 10 years. The larger call centers for Medicare plans have already had to do this for years. Starting October 1, that rule is being expanded to independent agents and brokers also. The other change is that an extra disclaimer will need to be said verbally in the first 60 seconds of any phone call in the enrollment process and it must appear on all websites and written communication. Here is the disclaimer: · “We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.” Here are a couple clarifications on that disclaimer: First, medicare.gov is one of the tools we use when comparison shopping with you. Also, the tools we use to compare Medicare plans allow us to show all the plans that exist in your area, not just our contracted plans, so we’re never hiding any available plans from you. We contract with most Medicare plans. There are some insurance companies that don’t sell their plans through independent agents, so we can’t be contracted with those. In the rare instances when the best plan for a Medicare beneficiary is one that we don’t contract with, we tell the beneficiary that. Honesty is the best way to stay in business for over 45 years. Have Medicare Questions? We Can Help!For answers to your specific Medicare questions and to objectively compare all available Medicare plans where you live, please feel free to call our office at 877-312-1414 or schedule a free, no obligation Medicare plan consultation. Our services are always free and enrolling through our office does not increase the cost of any insurance. 2023 Medicare Changes: Be Prepared for What's ComingOur goal is always to help you find the best value in Medicare coverage. Many changes are coming to Medicare in 2023 that may affect your coverage and your costs. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To... In this video, we’re taking a look at the Medicare changes for 2023 so you’ll know how these changes will affect you and be prepared for the Annual Enrollment Period between October 15 and December 7 when you’ll see these changes implemented in the 2023 Medicare Advantage and Part D plans in your area. By the end of this video, you’ll know how the changes to Medicare in 2023 that have been announced already will affect you and, just as important, I’ll tell you what to watch for in future months as even more 2023 Medicare rules and costs are released. Medicare Enrollment Period ChangesMedicare Initial Enrollment Period ChangesThere’s good news for anyone who will be enrolling in Medicare in 2023! For most people, the first time you’re eligible to enroll in Medicare is during your Initial Enrollment Period, which is a 7 month window surrounding your 65th birthday: three months before your birth month, your birth month, and three months after your birth month. Through the end of 2022, if you apply for Medicare before the month in which you turn 65, your coverage starts the first day of the month in which you turn 65. If you wait to enroll until the month of your 65th birthday, your coverage will start the next month. But what happens if you wait to enroll until months 6 or 7 of your Initial Enrollment Period? As the system is set up now, you do not have coverage starting the month after you apply. You have a penalty delay of coverage built in. Starting in 2023, that delay is going away. So if you wait to enroll in Medicare until those final months of your Initial Enrollment Period, your coverage will start the first day of the month after you apply. No more delay in coverage. Medicare General Enrollment Period ChangesThis enrollment period doesn’t affect many people. This is for anyone who missed their entire Initial Enrollment Period, which doesn’t happen that often. But if you miss your Initial Enrollment Period and want to enroll in Medicare later, you have to enroll during the General Enrollment Period. Here’s how that works right now. You enroll in Medicare between January 1 and March 31. Then your Medicare coverage starts on July 1. That coverage delay is also going away. Starting in 2023, the General Enrollment Period will still be January 1 through March 31, but your coverage will start the first day of the month after you apply. If you did not have creditable health coverage and waited until the General Enrollment Period to apply for Medicare, you may have late enrollment penalties, but you don’t have to wait months and months for your coverage to start. There are also some new Special Enrollment Periods that are being created in 2023 for people affected by exceptional circumstances. Here is a link to more information on those. Medicare Enrollment Due to Disability Before Age 65If you are eligible for Medicare due to a disability before age 65, your situation is different. Please see the video linked here for more information on your enrollment periods. Changes in Medicare Part D Vaccine Costs to YouMedicare vaccine coverage is a bit confusing. Some vaccines are covered by Medicare Part B and others are covered under Medicare Part D. For the vaccines covered by Part D, currently you run those charges through your Medicare Part D insurance. If you have a deductible to pay for the year or a copay or coinsurance for the vaccine, you have to pay that. Beginning in 2023, there will be no cost sharing for adult vaccines covered under Medicare Part D. That means your Part D covered vaccines will cost you nothing out of pocket. For this benefit you do have to have Medicare Part D coverage. If you decided not to take Part D, then you can’t take advantage of this vaccine benefit unless you enroll in a Part D plan. The most common vaccine this change will affect is the shingles vaccine. On most Part D plans the shingles vaccine has a significant copay, so this change will be a savings for anyone getting the shingles vaccine. Insulin Cost Sharing Limit of $35 per MonthThere’s already a program that some Part D plans participate in that limits your copays on insulin to $35 per prescription per month. Beginning in 2023, that will be expanded to every Part D plan and insulin covered under Medicare Part B. That means whether you use syringes or an insulin pump, you will have that $35 per insulin prescription per month cost sharing. Medicare Part D 2023 Projected Basic Part D Average PremiumThe basic Part D average premium is not necessarily the premium you pay to have Part D coverage. This number is released every year by CMS to give Medicare beneficiaries a very rough guide to the direction Part D are going in the new plan year. In 2022, the basic Part D average premium was $32.08. The 2023 basic average premium is $31.50. That’s a slight decrease that may be reflected in your plan options for Part D coverage in 2023, but doesn’t mean your current Part D plan is going to lower its premium. This number does affect those who have to pay the Part D late enrollment penalty. For more information on how that penalty is calculated, please see the video linked here. Medicare Insurance Plan Broker/Agent Communication ChangesTwo big changes are coming October 1, 2022 that will carry into 2023 regarding your communication with your Medicare plan agent or broker. The first change is that all phone calls between you and your Medicare plan broker that discuss Medicare Advantage plans or Medicare Part D coverage will have to be recorded and kept on file for 10 years. The larger call centers for Medicare plans have already had to do this for years. Starting October 1, that rule is being expanded to independent agents and brokers also. The other change is that an extra disclaimer will need to be said verbally in the first 60 seconds of any phone call and it must appear on all websites and written communication. Here is the disclaimer: “We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.” That disclaimer wording is a little odd, so I want to clarify a few things. First, medicare.gov is one of the tools we use when comparison shopping with you. Also, the other tools we use to compare Medicare plans allow us to show all the plans that exist in your area, not just our contracted plans, so we’re never hiding any available plans from you. We contract with most Medicare plans. There are some insurance companies that don’t sell their plans through independent agents, so we can’t be contracted with those. When the best plan for a Medicare beneficiary is one that we don’t contract with, we tell the beneficiary that. Honesty is the best way to stay in business for over 45 years. Medicare 2023 Changes Still to Come…The big change to watch for is the 2023 Medicare Part B monthly premium. Between 2021 and 2022, Medicare Part B had its biggest premium increase in history. A lot of that increase was due to a new very expensive Alzheimer’s medication that has since not lived up to expectations. Will CMS decrease the Part B premium for 2023? Keep it the same? No one knows yet. Here is a link to the most recent press release on Part B premiums, but don’t expect the final numbers to be released for a few months at least. Other 2023 Medicare information to watch for includes: IRMAA – the income related monthly adjustment amount for high income Medicare beneficiaries; and Medicare Parts A and B deductibles, copays, and coinsurance. One of the most important for you: specific plan changes to your current coverage. This is information you will receive in the next six weeks or so in your Annual Notice of Change (ANOC) document. This will tell you how your Medicare Advantage or Part D plan is changing for 2023. If any of those changes will negatively affect you, you will definitely want to compare your current plan to others in your zip code during the Annual Enrollment Period between October 15 and December 7. Have Questions? We Can Help!For answers to your specific Medicare questions and to objectively compare all available Medicare plans where you live, please feel free to call our office at 877-312-1414 or schedule a free, no obligation Medicare plan consultation. Our services are always free and enrolling through our office does not increase the cost of any insurance. How to Apply for Medicare: What to Do So You Don't Miss the Benefits You've EarnedThere are many ways to apply for Medicare benefits. Find out what you should do so you don't miss out on the benefits you've earned. And just as important, learn how to avoid Medicare late enrollment penalties. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

For answers to your specific Medicare questions and to objectively compare all available Medicare plans where you live, please feel free to call our office at 877-312-1414 or schedule a free, no obligation Medicare plan consultation. Our services are always free and enrolling through our office does not increase the cost of any insurance.

Medicare Eligibility

You are eligible for Medicare if you are

If you or your spouse worked and paid Medicare payroll taxes for at least 10 years, you qualify for premium-free Medicare Part A. If you paid Medicare payroll taxes for less than 10 years, you may still qualify for Medicare, but you will have to pay a monthly premium for Medicare Part A. Here is a link to more information on what your Medicare Part A premium will be if you are in this situation. How to Apply for Medicare Now, we’re going to look at how you enroll in Medicare. This is not the same for everyone. How you apply depends on when you take Social Security and whether you have continuing access to group health insurance. More info... If you are Turning 65 and Taking Social Security If you started taking Social Security before age 65 or applied to start taking Social Security at age 65, you will automatically be enrolled in Medicare Parts A and B. Your Medicare ID card will arrive in the mail a few months before you turn 65. If you will not have other health insurance at age 65, such as from a group employer health plan, you keep that Medicare card and comparison shop for Medicare coverage from Medicare Advantage, Medicare Part D, and Medicare Supplement carriers in your zip code. You will want to enroll so that your Medicare plan coverage starts the same date as your Medicare Parts A and B effective date. More info... If you have the option to keep a group health plan, through your or your spouse’s employer or some other source, you have some extra issues to consider. Here’s how to decide whether to stay with your group plan or go with Medicare for health coverage. The first thing to find out is whether your group plan is considered creditable coverage by Medicare. The HR department or benefits administrator will be able to give you that information. Generally, if your employer group plan covers more than 20 employees, it is considered creditable coverage by Medicare, but it’s always a good idea to check. If your employer plan is not creditable coverage for Medicare, you are usually better off going with Medicare coverage to avoid late enrollment penalties and save on overall costs. If your group plan is creditable coverage for Medicare, compare your group health costs and benefits with available Medicare plans in your area. In the past, group health insurance was usually a better deal financially for people turning 65, but that isn’t the case anymore. More than half the people we’ve spoken to in the last couple years have saved money and gotten better coverage by leaving their group plan and enrolling in Medicare and Medicare plans instead. If your creditable coverage group plan is better in terms of costs and benefits than any available Medicare plans in your zip code, you will want to decline Medicare Part B by calling Social Security. There are two reasons to decline Part B.

Most people who stay on a group health plan keep Medicare Part A even if they decline Part B. Part A has no monthly cost if you worked ten years and paid Medicare taxes during that time. The only reason to decline Part A in addition to Part B is if your group health plan is a qualified high deductible plan with a Health Savings Account. You can’t contribute to a health savings account once you’re on any part of Medicare, so if you would like to continue with your employer plan that has HSA contributions, you should decline both Medicare Parts A and B. If Medicare plans in your area are better than your group coverage, you will want to keep your Medicare ID card and Medicare Parts A and B and enroll in the Medicare plan or plans of your choice to start when your Medicare eligibility begins. Turning 65 and Delaying Social Security If you are not taking Social Security at or before age 65, you will not be automatically enrolled in Medicare. You will need to apply for the Medicare Parts and plans of your choice. You can do that beginning three months before your Medicare eligibility date. I recommend doing this as early as possible. Processing Medicare applications has been taking much longer than usual this year. You are eligible for Medicare on the first day of the month in which you turn 65. If your birthday is the first day of the month, your Medicare eligibility starts on the first day of the month before you turn 65. You can apply for Medicare online at ssa.gov/benefits/medicare, by calling Social Security at 800-772-1213, or at a local Social Security office. If you have the option of remaining on a group plan, you will want to go through the same decision process noted earlier to figure out which, if any, Medicare parts and plans are best for you. If you are declining Part A and/or Part B because of group creditable coverage, you can note that on the Medicare application with Social Security. If you will not have group coverage available once your Medicare coverage begins, you will want to apply for both Medicare Parts A and B and then comparison shop for the appropriate Medicare plans that best fit your financial and healthcare needs. These include Medicare Supplements, Medicare Advantage plans, and Medicare Part D plans. If you do not have other creditable prescription medication coverage, you will want to enroll in a plan that has Part D coverage, even if you do not take any medications, to avoid the Part D late enrollment penalty later. Under Age 65 Medicare Disability If you are under age 65 and have been entitled to Social Security or Railroad Retirement Board disability payments for 24 months, you will be eligible for Medicare and typically you will be automatically enrolled in Medicare Parts A and B. If you have ALS or permanent kidney failure, your Medicare eligibility starts immediately at diagnosis with no waiting period. The Medicare Part B premium will start to be deducted from your monthly Social Security benefits once Part B coverage is effective. If you have group health insurance that you can keep once your Medicare coverage starts, you should compare the group plan with available Medicare options as discussed earlier. If you don’t have group coverage, you will want to look at the Medicare plans in your area. Medicare Supplements, Medicare Part D, and Medicare Advantage plans are available to people who are under age 65 and on Medicare. Questions? We can Help! If you have questions about applying for Medicare and Medicare plans, please give us a call at 877-312-1414 or schedule a no obligation Medicare plan consultation. Why Doesn't Medicare Cover Dental? Four Ways to Save Money on Dental Costs for Seniors!

Medicare does not cover most routine dental care. Dental procedures like cleanings, fillings, tooth extractions, dentures, implants, and x-rays are not covered by Original Medicare.

In this post, we’ll go through four different ways to save money on your routine dental care when you’re on Medicare. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

Why Doesn’t Medicare Cover Dental?

When Medicare began in the 1960s, most health insurance didn't include dental coverage. The American Dental Association, the dentists, opposed including dental coverage in Medicare. This wasn’t seen as strange at the time since it was standard for medical insurance to not include dental. Now, dental coverage is pretty standard in employer group health plans and individual health plans, but Original Medicare still doesn’t include it. Over the years, Congress has tried to increase Original Medicare coverage, but due to the increases in costs to Medicare beneficiaries associated with added coverage, voters have rejected increasing levels of coverage to Medicare Parts A and B. If you are turning 65 or are over age 65 and leaving employer health insurance for Medicare, what options do you have for dental coverage? 1. Standalone Dental Plans Standalone dental insurance plan premiums can be as low as $10 a month up to over $80 a month, depending on the plan. Benefits and networks also vary widely. At the lower monthly costs, you can expect things like oral surgery, dentures, root canals, crowns, and orthodontia to not be covered at all. Standalone dental insurance plans have a maximum limit on how much they will pay for your dental care in a calendar year. With most plans, this limit is somewhere between $1000 and $5000. Many of these plans will not pay for major dental procedures, like implants, until you’ve been on the plan for 12 months, unless you are coming from prior dental insurance. Some dental plans also have graduated benefits. For example: plans pay for 60% of a service in your first year on the plan, then 80% the second year, and 90% the third year and following. Most standalone dental plans do use networks of dental providers, though some allow you to use any provider and reimburse you when you turn in a dentist’s bill. All the details of each dental plan are important to look at before enrolling so you can make sure you’re really getting a plan that will be valuable for you. If you would like assistance with plan comparisons, we can help. The annual maximum and the likely amount of benefits you’ll use are important considerations when comparing standalone dental plans. If you are going to be paying, say $50/month ($600/year), for an annual maximum benefit of $1000 or $1500, is that a good use of your hard-earned money? Or if you’re paying $80/month for a plan with an annual maximum benefit limit of $5,000, and realistically you’ll only need $750 a year in benefits, does it make sense to spend that $960 in premiums? Fortunately, standalone dental plans are month to month contracts that you can change, drop, or add anytime. You are not locked into a plan, so if what you have now isn’t serving you well, you can find something better and change. Cash Option Another option may be to put money in a savings account every year and use it to pay for dental expenses when they occur. Some dental offices offer discounts to patients who have no dental insurance but pay cash for services, so it’s a good idea to speak with your dentist’s office as part of your dental coverage decision making process. 2. Combination Dental Plans Some insurance companies offer combination plans that include dental and vision, or dental, vision, and hearing coverage all in one plan. If you are looking for benefits for routine vision care and hearing exams and hearing aids, combining everything with your dental insurance in one insurance policy can make sense. These plans do have annual maximum benefit limits for each type of coverage, so you’ll want to find a plan that has enough coverage for your needs in dental, vision, and hearing care. The combination plans usually also use networks of providers, so check the associated network for your dentist, eye doctor, and audiologist before enrolling. The costs for the combination plans are higher than standalone dental insurance, so again, it makes sense to estimate how much you are likely to use in benefits to see if what you’ll spend in monthly premiums for the insurance is worthwhile. 3. Dental Discount Programs These programs are not dental insurance, but they can lower your costs significantly. If you have a Medicare Supplement plan, you may already have a dental discount program included with that policy. There are also independent dental discount programs you can enroll in. These programs do have an annual cost to be in the plan. You can expect to pay about $120 for the year to be in the discount program. You will need to use dentists who contract with the discount plan for dental services. Those dentists have agreed to discount their rates by 15-60% for discount plan members. Because these are not insurance policies, the discount company doesn’t pay anything for your dental care. The company negotiated discounts with dentists, and you pay your membership fee to access those discounts. The discount programs have no waiting periods for major services like crowns or implants and no annual maximum benefit limits, since the discount company isn’t paying out any benefits. What’s the best dental coverage solution? That answer is unique to you. If you prefer a Medicare plan that doesn’t have a dental discount program, then we can look at the options for dental coverage available in your area, including possible discounts for cash payment with your current dentist, compare the pros and cons of every option, and then you choose the one that will work best for you. And, because most standalone dental insurance and discount plans are month to month contracts, you are free to change your mind anytime during the year. Curious about the dental options to you? Give us a call at 877-312-1414 or schedule a free, no obligation Medicare plan consultation. We’re happy to help you find the best value for your premium dollar! 2022 High Deductible Medicare Supplement Plan G: Can this Medigap Plan Save You Money This Year?Our goal is always to find you the best value in Medicare coverage. This year that’s more important than ever with the big increases to Medicare premiums and the state of the economy. Today, we’re talking about one particular Medicare Supplement plan, High Deductible Medicare Supplement Plan G. Medicare Supplements are also called Medigap plans, so just know that if you see either term, they mean the same thing. High deductible plans offer a much lower monthly premium cost than more comprehensive Medicare Supplements because they put more financial out-of-pocket risk on you for your medical care. High Deductible Medicare Supplement Plan G can save you a ton of money if you are a good fit for the plan. By the end of this video, you’ll know whether High Deductible Medicare Supplement Plan G is a good option for you. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

How does High Deductible Plan G work?

The premium cost for this plan is much lower than a standard Plan G. Like every other Medicare Supplement plan, High Deductible Plan G monthly premium cost varies from company to company and is based on where you live, your age, and other factors. In the Chicago area, for a 65 year old female, the High Deductible Plan G rates are between $40 and $70 per month, as of the date of this video. Monthly premium costs for a 65 year old female for a standard Plan G in the same area range from $108 to $160. Clearly, the premium savings of going with the High Deductible Plan G are pretty big. BUT What about the deductible? In 2022, the deductible amount that you pay before the High Deductible Plan G pays anything is $2,490. Does that mean you are paying for the first $2,490 in medical costs for the year? No, it does not. Medicare Parts A and B are your primary health insurance. A Medicare Supplement plan is secondary insurance. Medicare Parts A and B pay their claim responsibilities right from the beginning for any covered medical treatment you receive. What you are responsible for are the Medicare Parts A and B deductibles, copays, and coinsurance amounts up to $2,490 during the year. For outpatient care, you are responsible for the Part B annual deductible of $233. If you reach and pay that, then Medicare Part B generally pays for about 80% of covered outpatient care, leaving your responsibility at about 20%. The inpatient side of things is different. The Medicare Part A deductible is $1,556 per benefit period. After that Part A benefit period deductible is reached, you do have per day charges, should you have a very long hospital stay or skilled nursing facility stay. If you reach $2,490 in spending on covered medical treatment for the year, the High Deductible Plan G kicks in and pays claims just like a regular Standard Plan G. What that means in most cases is that, as long as all your medical care is covered by Medicare, after you’ve reached $2,490, you won’t have to pay any more besides your monthly premium for the rest of the year. Is High Deductible Plan G a good fit for you? It certainly might be! Choosing the right plan for you comes down to evaluating your unique situation. If you are pretty healthy and don’t need much medical care and have savings to cover the $2,490 deductible just in case of a catastrophic event or illness, then a High Deductible Plan G can be a great way to save money on your monthly premium costs. Medicare Supplement premiums do usually go up every year, but not every plan has the same percentage amount of increase. High deductible plans have much smaller increases than the more comprehensive plans, like standard Plan G, so not only will your premiums with High Deductible Plan G start much lower, they will also go up much more slowly. If you don’t make many office visits and aren’t hospitalized most years, your savings with a High Deductible Plan G will be substantial, due to the lower monthly premiums and smaller rate increases. If you have a serious or chronic condition that requires many office visits or in office treatments, a High Deductible Plan G may not be a good value for you. If you will be paying all or most of the $2,490 deductible in medical bills every year, that wipes out the savings in monthly premium. In that case, you would be better off with something more comprehensive, like a Plan N or standard Plan G. Changing Medicare Supplements Sometimes people are told that the Medicare Supplement plan they purchase at age 65 is the one they have to keep for life. That’s really not true. All types of Medicare plans allow you to move from one plan to another. There are rules to follow when changing, but we’re here to help you with navigating those rules to make plan changes. If you are healthy at age 65 and want a High Deductible Plan G, you aren’t locked into that plan forever. If your health does change in future years, making High Deductible Plan G no longer a good option for you, it is possible to change your coverage. The laws vary widely from state to state for changing Medicare Supplement plans. We will walk you through what rights you have to change Medicare Supplement plans in your state, so you can be confident in your choice and know that you aren’t stuck in any plan. Questions? We Can Help! If you’d like to see what High Deductible Plan G rates are in your area, please feel free to give our office a call at 877-312-1414, or schedule a free, no obligation Medicare Plan Consultation. Medicare Supplement Plan G: Is It the Best Medigap Plan??? Pros, Cons, Costs, and AlternativesLearn about Medigap Plan G coverage and costs and how to figure out if Plan G is the best Medicare Supplement option for you. We go through the pros, cons, and alternatives to this popular Medicare Supplement plan. Confused about your Medicare coverage options? Watch our free video: How to Find the Best Medicare Coverage Without Paying More Than You Need To...

Medicare Supplement Plan G Coverage

Medicare Supplement, also known as Medigap, coverage is standardized by law. So a Plan G from any company will have exactly the same benefits. Medicare Parts A and B are your primary health insurance. Medicare Supplements are secondary insurance. With standard Medicare Supplements, there are no networks, so you can use any doctor or medical provider who accepts Medicare. Plan G is the most comprehensive Medicare Supplement plan that can be purchased by anyone who enrolled in Medicare on or after January 1, 2020. For all medical care covered by Medicare Parts A and B, your out-of-pocket risk with a Plan G is limited to the Part B outpatient annual deductible. In 2022, this deductible is $233. If you reach that deductible, all covered outpatient expenses beyond that are covered at no cost to you between Medicare Part B and Plan G. This includes things like office visits, diagnostic testing, outpatient surgery, chemotherapy, and all other outpatient treatment. On the inpatient side, all covered expenses are split between Medicare Part A and Medigap Plan G. You have no out-of-pocket costs for inpatient care. This is one of the reasons why Plan G gets advertised as the best. It’s the most comprehensive. It has the most coverage and the lowest out-of-pocket risk to you. But there are trade-offs for that high level of coverage. Medigap Plan G Premium Costs and Rate Increases Because Plan G is the most comprehensive coverage with the least risk of out-of-pocket spending for you, it is the most expensive of the Medicare Supplement options in terms of monthly premiums. Since Medicare Supplement prices generally go up once a year as you age, we need to think about future costs in addition to the initial cost when you first apply. Plan G is more expensive when you first enroll, and you can expect yearly increases in the premium to be larger than what, say, a Plan N or High Deductible Plan G would have. Rate increases are partly based on aging and partly based on how much the insurance company pays out in claims. Every insurance company will pay out more in claims on Plan G than on less comprehensive Medicare Supplements, so Plan G rates will have higher percentage increases. For 65 year olds, Plan G is somewhere between $100 and $150 per month in most states. Every state has slightly different laws for Medigap plans. We’re going to look at the averages. If you live in a state that is a real outlier and has unique Medicare Supplement laws, your numbers could be significantly higher. Let’s also look at Plan N, which is one step down from Plan G in terms of comprehensive coverage. Plan N monthly premiums at age 65 are in the range of $75 to $130 per month. Not too much difference. However, you have to look at rate increases. In the past five years, Plan N rates have risen by about 2% per year. Plan G rates have risen by 6% per year. You can expect a small age increase every year and a percentage increase based on how much the insurance company paid in claims for people in your area in the same plan. Rate increases for usage are always based on a group of people, never on your individual medical claims. You can’t be singled out by the Medigap company for a rate increase. Once you’ve been on Medicare for several years, the difference in cost between Plan G and Plan N becomes significant due to those rate increases. Plan G still might be the better choice for you, but it’s important to be aware that those rate increases are coming. Is Plan G a good choice for you? If you have very expensive, ongoing treatments like chemotherapy, treatment for rheumatoid arthritis, diabetes, or any other medical condition that needs regular or costly treatment, a Plan G can be a good choice for you. That higher Plan G monthly premium is balanced out by the savings in out-of-pocket costs because you don’t have a big deductible to meet or any copays. If you want the peace of mind that your out-of-pocket risk is capped at the very low level of that Part B annual deductible of $233 and your budget can handle the Plan G monthly premium costs and rate increases, Plan G can be a good choice for you. If you are pretty healthy and don’t make many office visits in a typical year, it’s worth taking a look at Plan N or even High Deductible Plan G in addition to Plan G. Enrolling in Plan N or High Deductible Plan G can save you thousands in premium payments through your time on Medicare. More details on the differences in coverage and cost among Plans G, N, and High Deductible Plan G can be found here. Changing Medicare Supplement Plans You aren’t locked into a Medicare plan forever, so if you decide to change to or from a Medigap Plan G down the road, you usually can. Medicare Supplements generally require you to answer health questions to purchase a new Medicare Supplement once you’ve been on Medicare Part B for over 6 months, but there are exceptions to that rule. Medicare Advantage plans never require health questions to enroll. As your health or life changes, it’s a good idea to reevaluate your health insurance coverage to see if something else might be a better option. Why is Plan G marketed so much? Plan G is an emotionally reassuring option since it has such a small out-of-pocket risk, and the premium cost isn’t terribly high when a person is first looking for Medicare Supplement coverage at age 65. If an agent or broker never tells you about the future premium cost increases or calculates how much the insurance company is likely to pay out for your care compared to how much you will pay over the years in premiums, Plan G can seem like the best deal around. There are a couple other issues that play into some of the marketing push for Plan G. Because Plan G is the most comprehensive, it’s very easy to explain to clients and to new agents. Some agents, especially in big call centers, are trained to only sell Plan G because it’s a quick way to get a brand new agent selling. They learn one plan instead of dozens. Of course, that’s not in your best interest because one of those other plans the agent doesn’t know about could be the best coverage for your situation. Also, agent commissions are a percentage of the premium you pay. If you are paying a higher monthly premium, the agent makes more in commissions. This doesn’t necessarily mean an agent is trying to sell you something that isn’t a good choice for you, but always keep in mind that the more expensive plans benefit agents more. When you are looking for a Medicare plan agent or broker, you want to find someone who can explain and compare all plans that are available, not just the easiest to explain or the one that benefits the agent most. Questions? We Can Help! If you have questions about your Medicare coverage, please feel free to give our office a call at 877-312-1414 or schedule a free, no obligation Medicare Plan Consultation. . We objectively shop all available Medicare plans with you to find the best fit for your needs! |

How to Find the Best Medicare Coverage Without Paying More Than You Need To... Tabitha MoldenhauerLicensed health and life insurance broker since 2005 serving Alabama, Arizona, California, Colorado, Florida, Georgia, Idaho, Illinois, Indiana, Michigan, Minnesota, Missouri, North Carolina, New Hampshire, New Jersey, New Mexico, Nevada, Ohio, Tennessee, Texas, Utah, Virginia, Washington, and Wisconsin. Categories |

RSS Feed

RSS Feed